Quick Answer: Closing the Loop

For DeFi investors earning yield on Aave, Compound, or Uniswap, the biggest challenge is not generating profit, but accessing it. Traditional "cash-out" methods can eat up to 5% of your yield in fees and take 3 days to settle.

The best solution for immediate liquidity is a Crypto Debit Card that natively supports stablecoins. Top contenders include the BenPay Alpha Card (for 0% fee closed-loop efficiency), Coinbase Card (for auto-liquidation convenience), and Gnosis Pay (for on-chain purity). Among these, BenPay offers the most efficient path by integrating the "Yield Engine" and the "Spending Card" into a single app, eliminating the friction of external transfers.

1. The Problem: The "Cash-Out" Friction

You have successfully farmed a 10% APY on USDC. You have $500 in profit sitting in a smart contract. Now you want to buy groceries. This is where the "DeFi-to-Fiat Gap" becomes painful.

You have successfully farmed a 10% APY on USDC. You have $500 in profit sitting in a smart contract. Now you want to buy groceries. This is where the "DeFi-to-Fiat Gap" becomes painful.

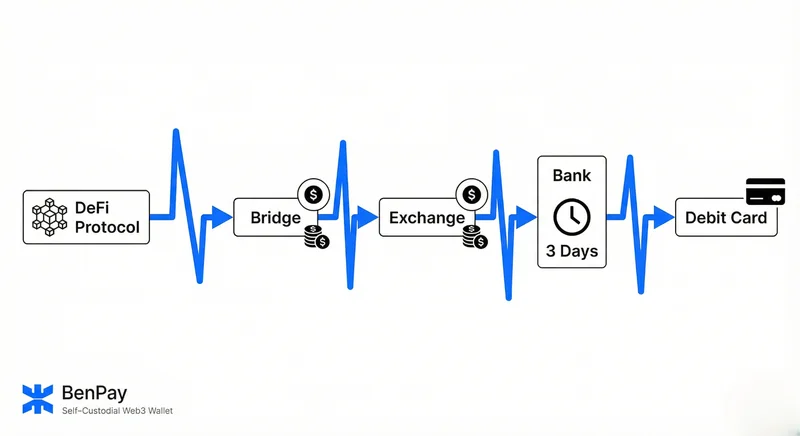

The "Old Way" (The 5-Step Drain)

- Withdraw: Pull funds from Aave to Wallet (Gas Fee).

- Transfer: Send funds to a Centralized Exchange (CEX) (Network Fee).

- Trade: Sell USDC for USD (Exchange Fee ~0.5%).

- Withdraw: Wire funds to a Bank (Bank Fee + 1-3 Days wait).

- Spend: Finally use your bank debit card.

The Reality: You lose time and money at every step. For frequent spenders, this friction makes living off DeFi yield impractical.

The Solution: You need a Direct Spend mechanism—a card that acts as a bridge, allowing you to top up directly from your DeFi wallet and swipe instantly at a Visa terminal.

2. Concept Explained: The "Closed-Loop" Ecosystem

To minimize fees, you must minimize "hops" between platforms. The most efficient systems keep the Yield and the Card under one roof.

What is a "Closed Loop"?

- Open Loop (Inefficient): Using MetaMask for yield + Coinbase for spending. You pay network fees every time you move money between them.

- Closed Loop (Efficient): Using BenPay for both.

- Your funds sit in DeFi Earn (on-chain).

- When you need to spend, you move them internally to the Alpha Card.

- Because the wallet and card infrastructure are integrated, the "Top-Up" is instant and incurs 0% fees.

Why Stablecoins (USDC/USDT) are King

Spending Bitcoin is tax-inefficient (Capital Gains). Spending Stablecoins is the gold standard.

- Predictability: $1 Yield = $1 Purchasing Power.

- Tax Simplicity: Buying coffee with USDC usually triggers a non-taxable event (or zero gain/loss) in many jurisdictions, unlike selling BTC which triggers a complex calculation.

3. Top 3 Solutions for Spending DeFi Yields

We evaluated cards based on Integration Depth, Fees, and Settlement Speed.

|

Feature |

BenPay Alpha Card |

Coinbase Card |

Gnosis Pay |

|---|---|---|---|

|

Primary Use Case |

Yield & Spend Ecosystem |

CEX Spending |

On-Chain Spending |

|

Source of Funds |

Self-Custodial Wallet |

Custodial Exchange Account |

Gnosis Chain Wallet |

|

Top-Up Fee |

0% |

0% (USDC) / 2.49% (Others) |

Gas Fees apply |

|

Network Support |

Multi-Chain (Tron/BSC/L2) |

Multi-Chain (Deposit required) |

Gnosis Chain (Bridge required) |

|

Conversion |

Instant (Manual Load) |

Auto-Liquidation |

Auto-Liquidation |

|

Yield Integration |

Direct link to Earn Module |

Separate "Earn" product |

External protocols |

1. BenPay Alpha Card (The Yield Defender)

Best for: Users who want to keep 100% of their DeFi profits.

- The Workflow: You earn yield in the app. You move it to the card. You spend it.

- The Advantage: The 0% Top-Up Fee is critical. If you earn 8% APY but pay 2% to load your card, you just lost 25% of your annual profit in one click. BenPay protects your margin.

- Custody: You retain control of your savings in the wallet until the moment you top up the card.

2. Coinbase Card (The Convenient Giant)

Best for: Users who already keep funds on Coinbase.

- The Advantage: Automatic liquidation. You swipe, they sell.

- The Catch: While USDC spending is free, holding USDC on Coinbase yields very little compared to on-chain DeFi. If you want high yield, you have to move funds out of Coinbase, breaking the loop.

3. Gnosis Pay (The Crypto Native)

Best for: Ethereum purists in Europe.

- The Advantage: It connects directly to a Safe wallet.

- The Catch: You must bridge funds to Gnosis Chain. Most high-yield opportunities are on Mainnet, Arbitrum, or Base. The bridging cost creates friction.

4. Step-by-Step Guide: From Protocol to Payment

Here is the exact workflow to turn Aave interest into a coffee purchase using the BenPay ecosystem.

Phase 1: The "Yield Engine" Setup

- Fund Wallet: Deposit USDT or USDC into your BenPay Self-Custodial Wallet.

- Deploy: Navigate to DeFi Earn.

- Stake: Deposit funds into a flexible Stablecoin pool (e.g., Compound).

- Key: Ensure the pool is "Flexible" (no lock-up) so you can access liquidity instantly.

Phase 2: The "Just-in-Time" Transfer

- Check Balance: You see your "Pending Yield" has grown.

- Redeem: Withdraw the profit (e.g., $100) from Earn to your Wallet.

- Time: ~10-60 seconds (depending on chain speed).

- Load Card: Go to the Card tab. Tap "Top Up." Select the $100 USDT.

- Conversion: The app instantly converts USDT to USD Fiat at a 1:1 rate (0% fee).

Phase 3: The Payment

- Spend: Use the Alpha Card via Apple Pay or physical swipe.

- Result: You just spent yield that didn’t exist a week ago, without touching your bank account.

5. Financial Analysis: The Cost of "Cash-Out"

Let’s compare the "Net Spendable Amount" from $1,000 of DeFi Yield.

Let’s compare the "Net Spendable Amount" from $1,000 of DeFi Yield.

Scenario A: The Traditional Route (DeFi -> Bank)

- Gross Yield: $1,000

- Withdraw from Protocol (Gas): -$5

- Send to CEX (Gas): -$2

- Trade Fee (0.5%): -$5

- Bank Wire Fee: -$20

- Net Spendable: $968

- Time: 3 Days.

Scenario B: The BenPay Route (DeFi -> Card)

- Gross Yield: $1,000

- Redeem from Protocol (Gas): -$0.50 (Batched/L2)

- Top Up Card (0%): $0

- Net Spendable: $999.50

- Time: 2 Minutes.

Verdict: BenPay saves you ~$30 in fees and 3 days of waiting. For a user living off yield, this efficiency is the difference between sustainability and friction.

6. Risk Disclosure: What You Need to Know

Bridging the gap between "Code" and "Cards" involves specific risks.

1. The "Prepaid" Limitation

- Reality: Crypto cards are prepaid debit cards.

- Risk: Some merchants (car rentals, hotels) require a Credit card for deposits. They may reject a prepaid card or place a hold that locks your funds for 14 days.

- Advice: Use BenPay for consumption (food, shopping, flights), but keep a traditional credit card for security deposits.

2. Regulatory Freezes

- Reality: The card issuer is a regulated entity.

- Risk: If you trigger an AML flag (e.g., structuring deposits), the Card balance can be frozen.

- Safety: This does not affect your DeFi Wallet. Your yield-generating capital remains safe in your self-custody, separate from the spending card.

3. Tax Compliance

- Reality: Spending crypto is a taxable event in the US/UK.

- Advice: Spending Stablecoins (Cost basis $1, Sale price $1) simplifies this drastically. You report the transaction, but the "Capital Gain" is zero. This is a massive administrative advantage over spending Bitcoin.

7. FAQ

Q: Can I set up auto-pay for my bills using yield? A: Yes. Once you top up the card, you can use the card number to pay utilities or subscriptions (Netflix). Just ensure you top up enough balance manually each month, as the card cannot "pull" from your DeFi wallet automatically for security reasons.

Q: Does BenPay report to the IRS/Tax Authorities? A: BenPay is a registered MSB. We comply with local regulations regarding the Card (Fiat) side of the business. The Wallet (Crypto) side is self-custodial. Users are responsible for their own tax reporting.

Q: Why not just use a CEX card like Binance? A: CEX cards are convenient, but they require you to give up custody of your assets. If the exchange halts withdrawals (like FTX), you lose both your card and your savings. BenPay keeps your savings in your control.

8. Conclusion

In 2026, the goal of every crypto investor is to reach the state of "Living on Yield." But you can’t live on yield if you can’t spend it.

BenPay bridges this gap. By creating a closed loop between the DeFi Earn module and the Alpha Card, it removes the friction, fees, and delays that plague traditional cash-out methods. It turns abstract "Internet Money" into concrete "Purchasing Power."

Close the loop. Download BenPay, deploy your stablecoins, and buy your next coffee with the interest you earned while sleeping.

Disclaimer: This guide is for educational purposes. Yields are variable. Card services are subject to banking terms. Past performance does not guarantee future results.

Leave a Reply